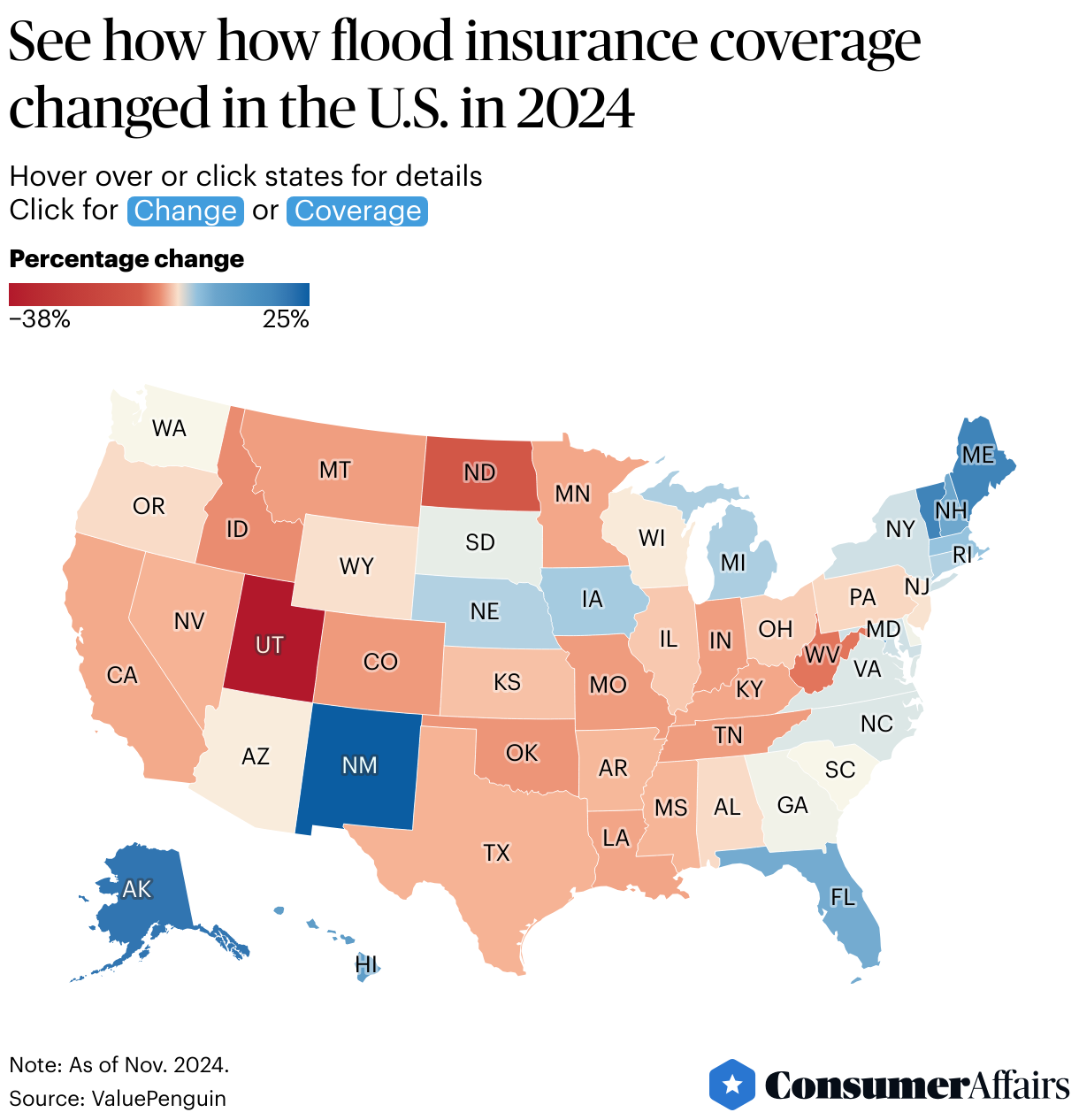

Utah had the biggest decline in coverage

A staggering amountof U.S. homes don't have flood insurance despite mounting fears of natural disasters.

Just 3.3% of U.S. homes had active National Flood Insurance Program (NFIP) policies as of Nov. 2024, marking a second-year of declines and a 0.2% drop from the prior year, according to a report from insurance website ValuePenguin.

NFIP policies account for the vast majority of flood insurance and provides thebasics, but a smaller share of homeshave private flood insurance that can offerbroader coverage.

"Two years of back-to-back decreases in active flood insurance policies indicates that many homeowners arent fully aware of the growing risks of flooding," said Divya Sangameshwar, ValuePenguin's insurance expert, in the report.

The situation is even worse in 26 states where less than 1% of homes have flood insurance, including Pennsylvania, Colorado and Michigan.

And 36 states saw a drop of flood insurance in 2024, led by Utah with a decline nearly 38%, followed by North Dakota with a drop of 10% and West Virginia with nearly 8%.

But homes in some states are buying flood insurance with the biggest jump in New Mexico.

The share of homes with policies in New Mexico surged by more than a quarter in 2024 after a severe storm caused widespread flooding in Oct. 2024 and led to a federal disaster declaration, ValuePenguin said.

New Mexico's increase in flood insurance is because recent natural disasters and the Federal Emergency Management Agency (FEMA) offering five years of coverage for homes that weren't required to carry it in some areas,Sangameshwar said.

"This raises awareness of the importance of protection against flooding," she said.

Florida, hit by Hurricane Helene in 2024, also saw a jump of above 3% in coverage.

Oher states where homes hadthe biggest percentage increases in flood insurance coverage were Alaska (21%), Maine (19%) and Vermont (18%).

In 2024, ValuePenguin said nearly 31% of losses from flood insurance were outside of FEMA's designated areas, showing how floods oftenhappen in low-risk areas where homeowners may want to get the insurance even when it might not seem necessary.

"Climate change continues to drive sea-level increases and make weather more extreme," Sangameshwar said. "As a result, flood-prone areas around the country are expected to grow by nearly half in just this century."

Tips on getting flood insurance

ValuePenguin'sSangameshwar has some advice for buying flood insurance:

- Floods happen in low-risk areas: "Even if flood insurance is only required for a small subsection of homeowners, low flood risk doesnt mean zero flood risk,"Sangameshwar said."And homeowners insurance and renters insurance dont cover flooding."

- No need to shop around: Flood insurance premiums through the NFIP are the same regardless of the insurer or agent you go through so you don't need to shop around.

- More coverage: Private insurers offer even more coverage, but this makes sense only for higher-value homes.

- Lower waiting periods: Private insurance has lower waiting periods of around 14 days, compared with around 30 for NFIP coverage.

- But private insurance can be risky:"Insurers could drop your coverage in the middle of your term or decline to renew it, leaving you scrambling for a new policy,"Sangameshwar said.

Sign up below for The Daily Consumer, our newsletter on the latest consumer news, including recalls, scams, lawsuits and more.

Posted: 2025-02-28 22:51:15