Some states are allowing lenders to charge eye-watering interest rates

The interest rates loans can charge varygreatly from state to state.

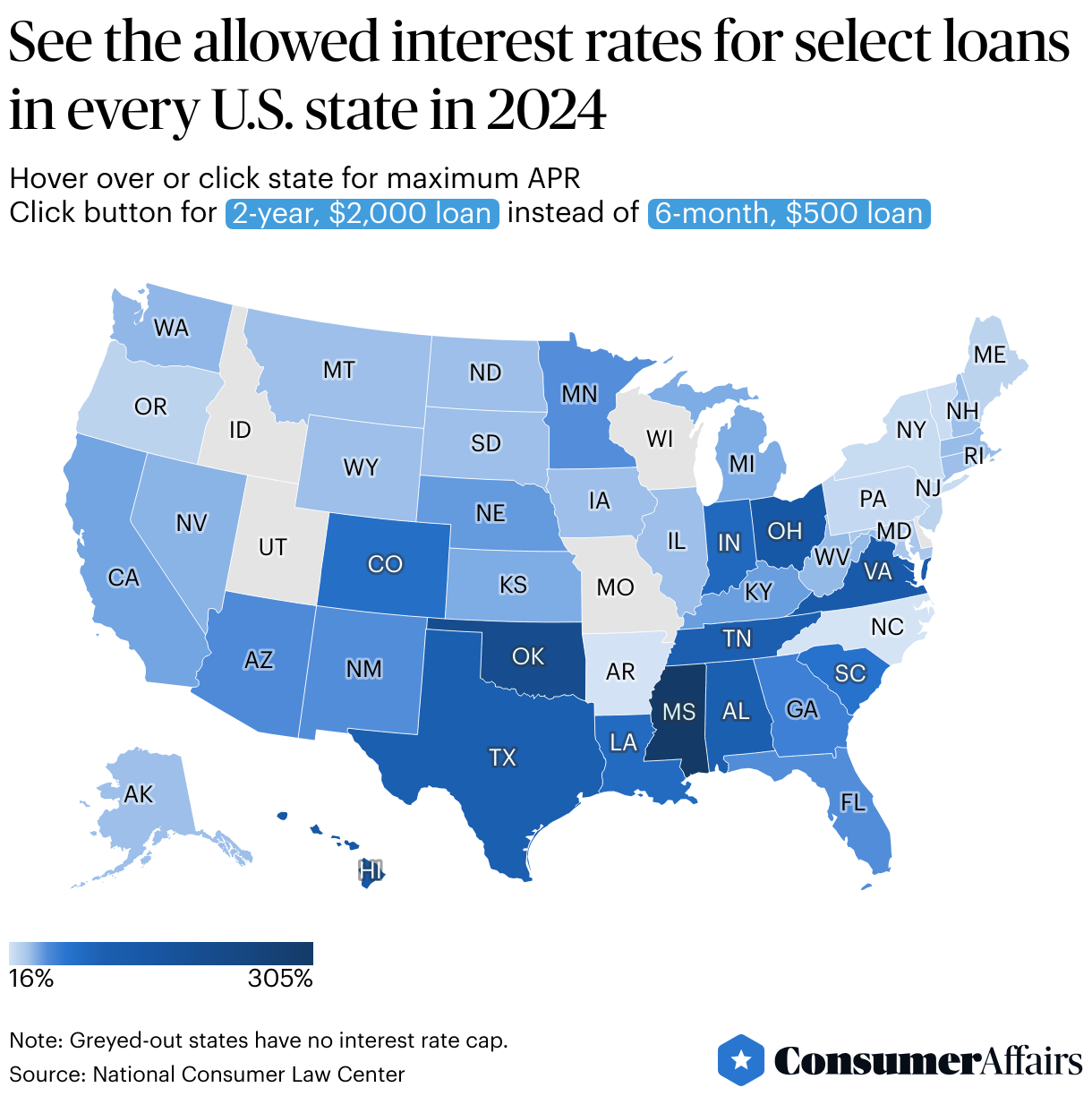

Fourty-fivestates plus the District of Columbia cap interest rates onat least some installment loans as of 2024, the National Consumer Law Center said in a report.

There's no federal law capping interest rates on loans, which leaves it up to the states to set their own rules.

The NCLC said it recommends a cap of no more than 36% for loans of up to $1,000 and significantly lower limits for larger loans.

There were 19 states, plus the District of Columbia,with APR caps between 16% and 36% for 6-month, $500 loans.

For 2-year, $2,000 loans, there were 32 states, plus the District of Columbia, with APR caps between 17% and 36%.

Still, many states are allowing lenders to charge muchhigher interest rates or don't cap rates at all.

Delaware and Missouri impose no capon 6-month, $500 loans or2-year, $2,000 loans.

Five statesAlabama, Idaho, South Carolina, Utah and Wisconsindon't set specific numbers for allowed APRs but have rules that forbid lenders from charging interest rates that are "unconscionable," which presents challenging legal avenues for borrowers.

Then there are the states that permit very high interest rates.

For 6-month, $500 loans, eight states allowed APRs above 100%: Mississippi (305%), Oklahoma (204%), Hawaii (146%), Ohio (145%), Virginia (129%), Texas (109%), Alabama (107%) andTennessee (106%).

For 2-year, $2,000 loans, eight states allowed APRs at 40% or above:Mississippi (59%), Oklahoma (54%), Virginia (50%),Tennessee (43%), Kentucky (42%), Arizona (41%), Indiana (40%) and Nevada (40%).

The NCLC said states that don't cap interest ratesor allow lenders to charge high APRs are harming borrowers and discouraging lenders fromseeingloans repaid.

"Excessive interest rates enable lenders to profit from loans even if many borrowers eventually default," the NCLC said."The lender has little incentive to ensure that each borrower can actually afford to repay the loan in full on its terms if the lender can be made whole even if the borrower defaults, or can recoup defaults from exorbitant rates on others."

On the other hand, there are states with stricter caps on interest rates.

For 6-month, $500 loans, eightstates and the District of Columbia capped interest rates at 30% or lower: North Carolina (16%), Arkansas (17%), Vermont (24%), District of Columbia (24%), New York (25%), Pennsylvania (27%), New Jersey (30%), Maine (30%) and Oregon (30%).

For 2-year, $2,000loans, eight states and the District of Columbia capped interest rates below 30%: Arkansas (17%), Vermont (21%), District of Columbia (24%), Pennsylvania (24%),Massachusetts (24%), New York (25%), California (25%), Rhode Island (29%) and Washington (29%).

Photo Credit: Consumer Affairs News Department Images

Posted: 2024-11-27 02:00:00