Severe weather is pushing insurance to the brink

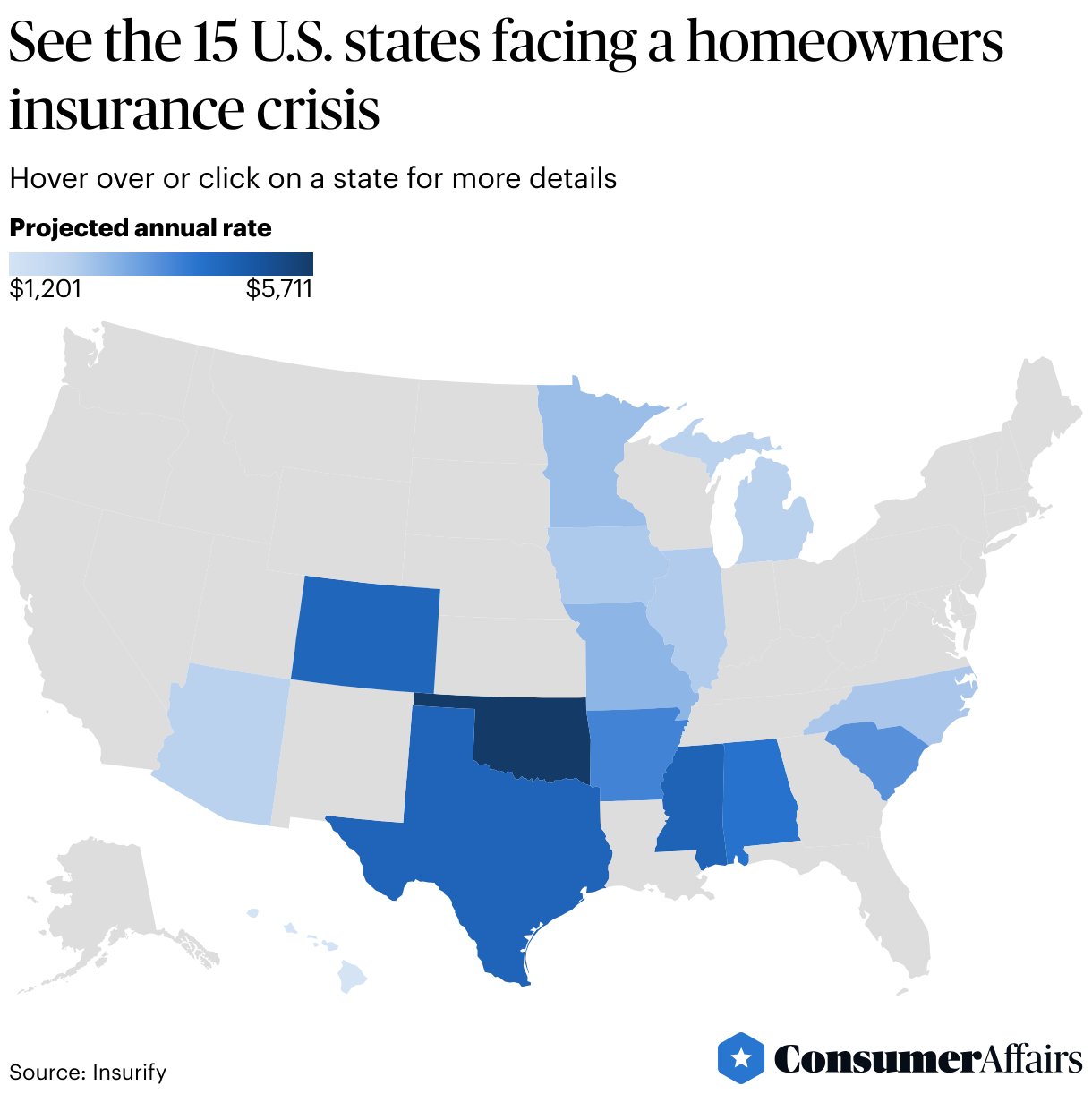

Headlines have focused on home insurers pulling out of California and Florida, but there are 15 other states that are facing an "imminent" homeowners insurance crisis, according to a report from insurance-comparison website Insurify.

The culprit is severe weather, such as flooding and hail, hiking up homeowners insurance rates and causing insurers to pull out of statesthat used to have low-cost, widely-available insurance.

"The 2020s have been the worst decade to date in terms of damages caused by severe weather and natural disasters," Chase Gardner, data insights manager at Insurify, told ConsumerAffairs. "It's also happening with smaller events likesevere thunderstorms across huge portions of the U.S."

Unless legislation tackles the problems and efforts are made to make communities more resilient to weather, homeowners can expect weather-related rate hikes and less competition among insurers in the states, Insurify said.

Insurify singled out the 15 states based on how insurers have been pulling back,increasing rates and conversations with insurers about concerns in the states.

The 15 states facing a homeowners insurance crisis are:

- Alabama

- Arizona

- Arkansas

- Colorado

- Hawaii

- Illinois

- Iowa

- Michigan

- Minnesota

- Mississippi

- Missouri

- North Carolina

- Oklahoma

- South Carolina

- Texas

Why are these states having problems with homeowners insurance?

The homeowners insurance crisis is spreading to more states because climate conditions are changing andlosses from weather continues to mount.

Michigan, which has the highest projected homeowners insurance increase of 14% in 2024, is seeing ice cover decrease on the Great Lakes that can cause more rainfall and flooding, Insurify said.

Insurer SECURA last year stopped offering personal lines of insurance in Michigan and several other states.

South Carolina, which comes second to Michigan with a projected increase of 11%, is suffering from the aftermath of Hurricane Helene, but homeowners were already paying 29% more than the U.S. average, Insurify said.

South Carolina used to have an average of $1.5 billion in individual weather events annually in the 1990s, but the 2000s has averaged at $5 billion, Insurify said.

State-run homeowners insurance providers, which are often a choice of last resort, are now taking on more clients than they can sustainably handle in the states after insurers have pulled out, Insurify said.

How have homeowners insurance rates been rising overall?

Homeowner insurance rates are expected to increase 6% in 2024, less than the around 12%uptick in 2023, Insurifysaid, but the hikes are still higher than the roughly 2% increases that took place in previous years.

"I wouldn't be surprised if rates kept rising faster than historical averages," Gardner said.

Since the 1980s, every decade has had higher damages from severe weather, even after adjusted for inflation, Garder said.

There was around $21 billion worth of damages from severe weather in the 1980s, but that number reached $123 billion just through 2023 from 2020, Gardner said, citing data from the National Oceanic and Atmospheric Administration.

This year isn't looking good either afterHurricanes Helene and Milton are expected to cause up to $47.5billionand $175 billionworth of damages, respectively, according to early estimates,CNBC reports.

"It's hard to say rates will return to a normal cadence," Garnder said.

Photo Credit: Consumer Affairs News Department Images

Posted: 2024-10-15 13:52:09