Homeowners in Miami and Houston are struggling more

Millions of American don't have homeowners insurance, exposing them to natural disasters and challenging their ability to build wealth.

One in thirteen, or 7.4%, of U.S. houses lacked homeowners insurance in 2021, according to an analysis by nonprofit Consumer Federation of Americaof the U.S. Census's most recent American Housing Survey.

That is the equivalent of around6.1 million homes and at least $1.6 trillion of uninsured property under conservative estimates, CFA said.

Not only are uninsured families unprotected, but the economic fabric of entire communities is also at risk if significant portions of residents cannot rebuild after a disaster," said Douglas Heller, CFAs director of insurance.

Foregoing homeowners insurance is often called "going bare," which comes at a timewhen Americans are struggling to pay steep premiums and getinsurance in somestates, such as California and Florida,that some insurers are pulling out of.

It is possible even more homeowners are uninsuredtoday after insurance costs have gone up in recent yearsand living comfortably has grown more expensivedue to inflation, but CFA said research into homeowners insurance remains in its infancy because ofpoor data.

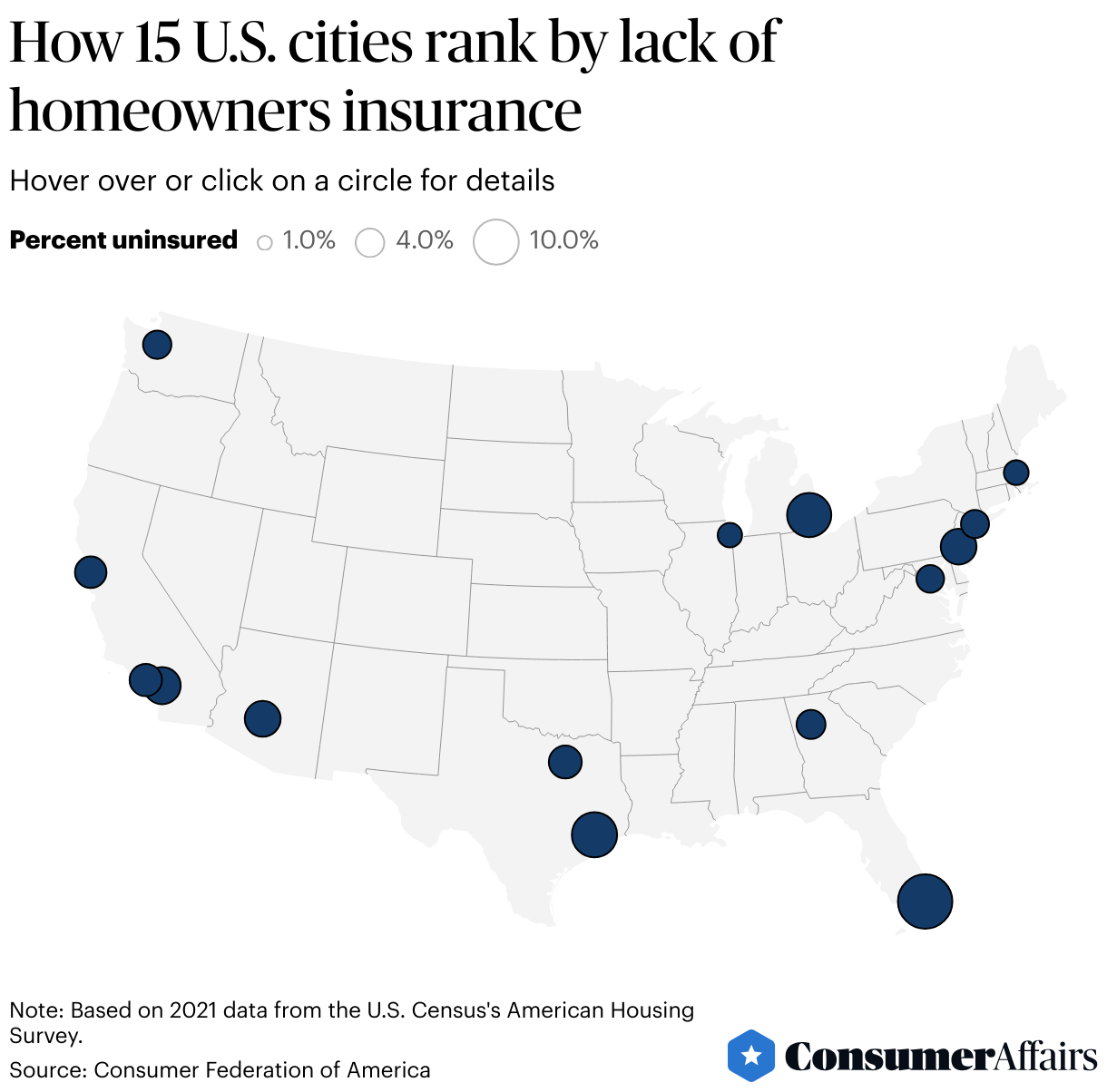

Where Americans don't have homeowners insurance

The disparity in homeowners insurance is on display among 15 of America's biggest cities.

In 2021, thefivecities with the highest percentageof uninsured homes wereMiami (14.5%), Houston (9.8%), Detroit (9.3%), Riverside (6.3%) and Phoenix (5.8%).

The fivecitieswith the lowest percentageof uninsured homes wereChicago (2.4%), Boston (2.5%), Washington D.C. (3.3%), New York City (3.4%) and Seattle (3.5%).

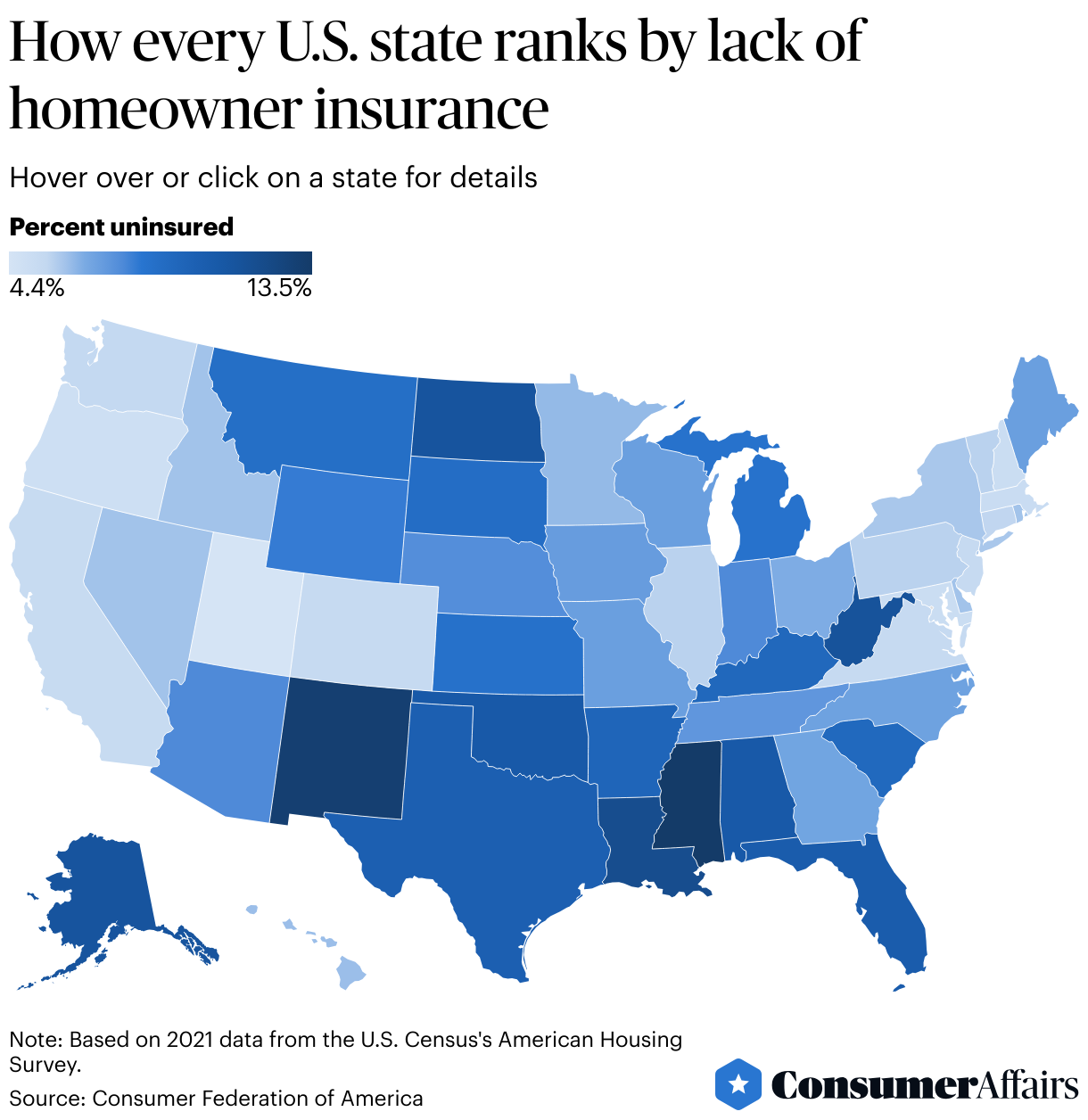

The percentage of homes with insurance variesconsiderably by city andstate, in large part because of household income, frequency of natural disasters and availability of competitively-priced insurance.

The five states with the highest percentage of uninsured homes wereMississippi (13.5%), New Mexico (13.1%), Louisiana (11.9%), West Virginia (11.3%) and Alaska (11.2%).

The five states with the lowest percentage of uninsured homes wereUtah (4.4%), Oregon (4.9%), Maryland (5.1%), New Hampshire (5.1%) andMassachusetts (5.2%).

How can homeowners insurance coverage be improved?

CFA has recommendations for what should be done to address the issue of homeowners insurance:

- More investment:Governments need to grow investments inprotecting communities and homes from natural disasters, which could lower what insurers charge.

- More data:Regulators need to collect more specific and timely information on homeowners insurance to understand where the problems are.

- Racialgaps:Homeowners of color are reportedly being denied insurance because of their ethnicity and more research needs to be done under existing Fair Housing Laws to hold insurers accountable.

Tips for lowering homeowner insurance premiums

The Insurance Information Institute has suggestions to lower your homeower insurance bill:

- Shop around:Compare multiple insurers, contact your state insurance department, check consumer guides, speak with insurance agents and use online comparison services to get a good price.

- Raise deductible:Increasing your homeowner insurance deductible, or what you pay towards a loss, from typically $500 to $1,000 can lower the amount you pay in monthly premiums.

- Bundle insurance:Buying both your car and home insurance from the same provider can get you a discount.

- Stay with insurer:Keeping the same insurer for several years can get you a discount as a long-term policyholder.

- Improve disaster resilience:You may be able to save on premiums by adding home upgrades such as storm shutters, reinforcing your roof and buying stronger materials.

- Improve security:Installing burglar alarms, dead-bolt locks, smoke detectors and fire sprinklerscan lower your monthly homeowners insurance premiums.

Photo Credit: Consumer Affairs News Department Images

Posted: 2024-09-17 07:48:28