Why? Well, youre holding on to that car of yours too long for one thing

Auto insurance rates have doubled in the last 10 years, according to the latest Consumer Price Index data and its outpacing inflation, putting an added financial strain on many Americans.

It seems like no matter what expert you speak to, their reason for this is different than the next persons. Heres what auto insurance savants told ConsumerAffairs...

Billboard attorneys

Breanne Armstrong, director of insurance intelligence at J.D. Power pinned the tail on billboard attorneys those blustering lawyers who take to social media, highway billboards, and TV ads promising that they can basically beat an insurance company into submission when someone has an accident.

This is causing the overall costs of claims to rise, resulting in premium increases being passed on to insurance customers, Armstrong said. She says that when those aggressive attorneys in states like Louisiana in a dead heat with New York for the most expensive state for auto insurance get involved and abuse the legal system, it can cost a person upwards of $1,100 a year.

And because weve gotten sue-crazy, those lawyers fees are as high as they have ever been, said Michael Collins, CFA, Founder and CEO of WinCapFinancial. Meaning going to court costs insurance companies much more now than in the past.

Fancy tech

Then, theres all the digitalbells and whistles that automakers have added to our cars and trucks. Those advancements may be cool, but repairing or replacing electronic and computer-based components can get very costly, says ClaimJournals Rick Gorvett.

Also, there is now more multi-component manufacturing, which promotes cost-effectiveness and efficiencies in the building process, but also results in greater costs associated with repairing or replacing a damaged component, since often the entire structure around that component must be replaced, he said.

Behaviorally, distracted driving is becoming an increasing problem[too]. Advancements in available technologiesphones, GPS, and other electronicstempt drivers attention away from focusing on the road.

Youre keeping your old car too long

You may love that 88 Dodge truck of yours, but the insurance companies think youre running a risk. Brian Williams, CEO of FIMC, a company that helps families manage common financial disruptions, including those from auto breakdowns, said that over the past few years, the surge in new and used car prices forced many families to keep their cars longer, from about 12 to 15 years.

Older cars require more frequent repairs, and supply chain issues have driven up the price of necessary parts. This increase in costs impacted both consumers and insurance companies, leading insurers to raise rates. Ultimately, however, it's consumers who are left to shoulder the expense, he said.

Theres more to an accident than just a dented fender these days

When ConsumerAffairs spoke to Hugh Allen, Principal Product Strategist at Hi Marley, a tool that allows insurers to connect and collaborate with policyholders via text, Allen said that auto accident frequency and severity have increased, resulting in more claims.

And these aren't your run-of-the-mill fix-my-bumper claims, either. Claims nowadays are for lots of other things like rental car costs for first and third-party claimants, and injury-related costs, such as medical bills. These costs ultimately get passed to consumers in the form of increased auto insurance premiums, Allen said.

If you think its bad now, just wait

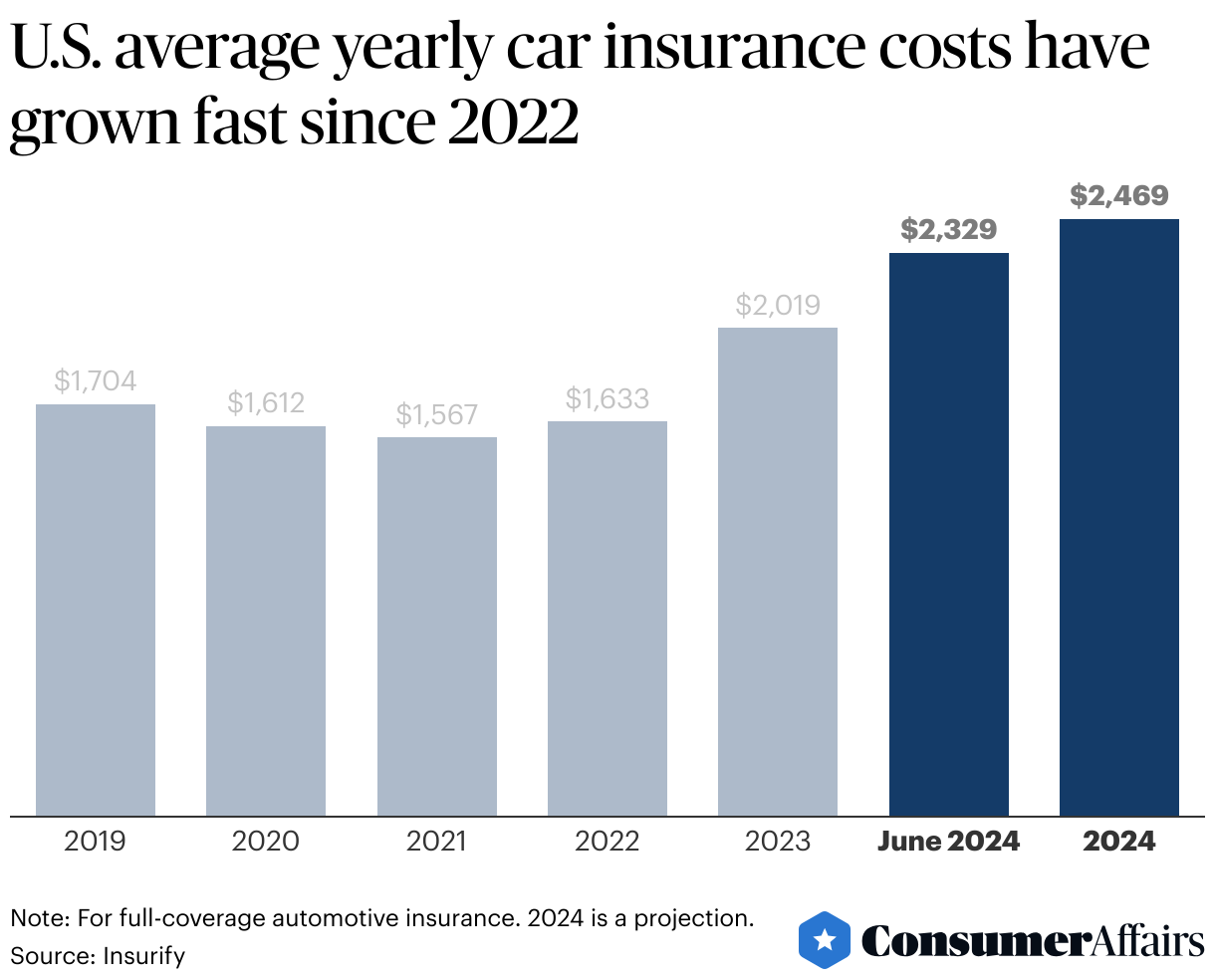

Car insurance rates skyrocketed after COVID, but experts predicted that wed have slower rates in 2024. Well, they blew that prediction. Data provided to ConsumerAffairs from the data science team at Insurify projects a total 22% increase by the time 2024 is said and done. Insurify says were sitting at $2,329, and predicts California, Missouri, and Minnesota could see car insurance costs increase by more than 50% in 2024.

If you want the full picture of what to expect in the way of projected auto insurance costs, take a look.

The reasons rates are climbing now is a mix of factors. One thing is that insurers have taken a record hit in underwriting losses $33.1 billion in the year prior, mostly due to the rising cost of vehicle repairs and the skyrocketing price of new cars.

But, theres also the unprecedented climate catastrophes that drive weather-related claims in states that havent historically seen as much of this type of damage in the past. Midwestern and Southern states are seeing an increase in severe storms, tornadoes, and flooding; youve got more wildfires in the Mountain and Western states; and in the Northeast, some of the regions that were considered safe are now dealing with more intense storms and rising sea levels which are causing damage further inland.

Photo Credit: Consumer Affairs News Department Images

Posted: 2024-08-15 16:51:55